TL;DR:

- Essential maintenance coverage combines equipment breakdown insurance with routine service plans to protect property systems from both sudden failures and gradual wear. Proper documentation of maintenance activities is crucial for claim approval, as insurers investigate whether damage resulted from neglect or an unforeseen event. Regular scheduling and record-keeping help homeowners and landlords ensure ongoing coverage and prevent costly claim denials.

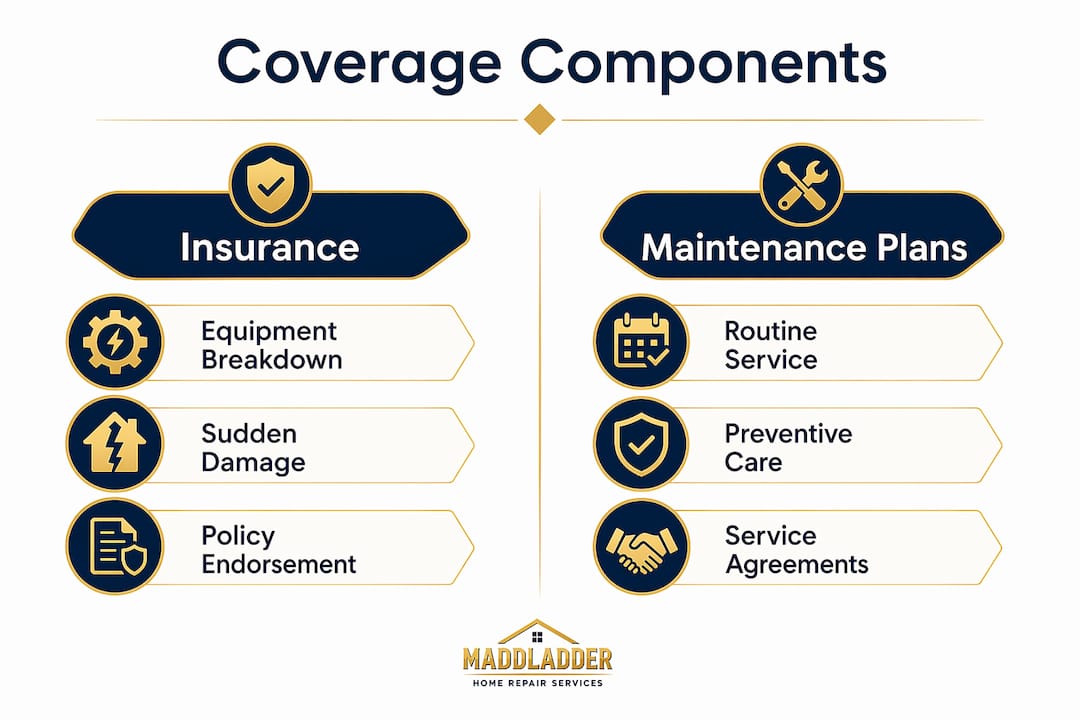

Essential maintenance coverage is the strategic layering of Equipment Breakdown insurance endorsements and routine service plans that protects your property's critical systems from both sudden failures and gradual wear. Standard homeowner policies exclude internal mechanical failures entirely, meaning a failed HVAC compressor or burst water heater can cost thousands out of pocket without the right coverage in place. Understanding what is essential maintenance coverage gives homeowners and landlords a clear framework for managing property risk before a breakdown becomes a financial crisis. The two components work together: insurance handles the unexpected, and maintenance plans handle the predictable.

What is essential maintenance coverage, and what types of plans does it include?

Essential maintenance coverage is not a single product you buy off a shelf. It combines two distinct protection layers that address different types of property risk.

The first layer is an Equipment Breakdown endorsement added to your standard homeowner policy. This endorsement covers sudden internal electrical or mechanical failures in systems like HVAC units, water heaters, electrical panels, and appliances. The key word is "sudden." If your furnace motor burns out without warning, that qualifies. If it slowly deteriorates because filters were never changed, it does not.

The second layer is a routine service plan, sometimes called a maintenance agreement or home care plan. These plans cover scheduled upkeep tasks: filter replacements, fluid checks, seasonal inspections, and minor adjustments. Service plans are not insurance and will not pay for catastrophic failures. They are a financial tool for managing predictable, recurring costs.

| Coverage type | What it covers | What it excludes |

|---|---|---|

| Equipment Breakdown endorsement | Sudden internal mechanical or electrical failure | Wear, neglect, gradual deterioration |

| Routine service plan | Scheduled upkeep, filter changes, inspections | Sudden failures, structural damage |

| Standard homeowner policy | Fire, storm, theft, liability | Internal mechanical failure, wear and tear |

Pro Tip: Ask your insurance agent specifically about an Equipment Breakdown endorsement. Many homeowners do not know it exists because standard policies never mention it.

Layering these two coverage types is industry best practice for fully managing property maintenance risk. Neither layer alone provides complete protection. Together, they cover the full spectrum from a burst pipe fitting to a twice-yearly HVAC tune-up.

Why does documentation make or break your maintenance claim?

Insurers do not take your word for it. When you file a claim, they investigate whether the damage was sudden or the result of deferred upkeep. That distinction determines whether you get paid.

Claim denials increase when homeowners cannot prove they performed scheduled maintenance. In 2025, claim rejections for damage linked to poor maintenance rose by 17.5%. That figure reflects a deliberate shift by insurers toward stricter scrutiny of moisture damage and deferred upkeep claims.

The practical implication is straightforward: your maintenance records are as valuable as your policy documents. Keep the following for every property system:

- Receipts and invoices from every service visit, including the date, technician name, and work performed

- Photographs taken before and after maintenance tasks, especially for plumbing, roofing, and HVAC systems

- Manufacturer maintenance schedules printed or saved digitally, showing what intervals are required

- Inspection reports from licensed contractors, particularly for electrical panels and water heaters

Missing maintenance records can result in a denied claim even when the work was actually done. An insurer cannot verify what you cannot document. This is especially true for slow leaks that cause rot or mold. Standard policies treat those as preventable and deny coverage as a result.

Pro Tip: Create a shared digital folder for each property. Store every invoice, photo, and inspection report there. If you manage multiple units, label folders by address and year.

Landlords face added complexity because tenants may not report small issues promptly. A property maintenance guide for landlords can help you build a system that catches deferred problems before they become denied claims.

What are the real benefits and limits of maintenance coverage?

The financial case for maintenance coverage is clear. Predictable monthly or annual plan costs replace unpredictable repair bills. A single HVAC replacement can run $5,000 or more. An Equipment Breakdown endorsement typically costs a fraction of that per year.

The benefits stack up across three areas:

- Reduced out-of-pocket exposure. Equipment Breakdown endorsements shift the cost of sudden system failures to your insurer, subject to your deductible.

- Budget predictability. Routine service plans convert variable repair costs into fixed, scheduled expenses. That matters for landlords managing cash flow across multiple units.

- Preserved insurability. Documented maintenance keeps your claims eligible. Skipping manufacturer-recommended service can void your Equipment Breakdown coverage entirely, as coverage applies only to sudden failures not caused by neglect.

The limits are equally real. Maintenance coverage does not pay for cosmetic damage, gradual deterioration, or items excluded from your specific policy. Wear and tear is not covered by standard insurance. That is the most common misconception homeowners carry into a claim. A roof that ages out over 20 years is not a sudden event. Neither is a water heater that corrodes slowly over a decade.

Service plans also have firm boundaries. They cover preventive upkeep, not repairs triggered by a failure event. Confusing the two leads to coverage gaps that cost money at the worst possible time.

How can homeowners and landlords put maintenance coverage to work?

Effective implementation starts with a property audit. Walk through every major system and note its age, condition, and manufacturer-recommended service interval. That list tells you where Equipment Breakdown endorsements add the most value and where routine service plans are most needed.

Selecting the right coverage layers

Evaluate your property's asset value before choosing endorsements. Older homes with aging HVAC systems, electrical panels, or water heaters carry higher breakdown risk. For those properties, an Equipment Breakdown endorsement pays for itself quickly. Newer construction may need less immediate coverage but benefits from establishing a maintenance plan early.

Subscription maintenance plans offer a structured way to manage recurring upkeep. Tiered plans let you match coverage depth to your property's needs. An entry-level plan might cover seasonal HVAC checks and filter replacements. A higher tier adds plumbing inspections, electrical checks, and exterior maintenance.

Building a maintenance schedule that protects your claims

Seasonal scheduling is the most reliable way to stay current on required maintenance. A seasonal maintenance approach catches problems before they escalate and keeps your documentation current throughout the year.

Key tasks to schedule by season:

- Spring: HVAC system inspection and filter replacement, roof inspection after winter, gutter cleaning, exterior caulking check

- Summer: Plumbing pressure check, attic ventilation inspection, pest inspection for wood-destroying insects

- Fall: Furnace tune-up, water heater flush, weatherstripping replacement, chimney inspection

- Winter: Pipe insulation check, sump pump test, smoke and carbon monoxide detector battery replacement

Landlords managing multiple properties benefit from a KC home maintenance checklist that standardizes tasks across units. Consistency across properties reduces the risk of missed maintenance and disputed claims.

| System | Recommended service interval | Documentation to keep |

|---|---|---|

| HVAC | Every 6 months | Service invoice, filter receipts |

| Water heater | Annually | Flush record, anode rod inspection |

| Electrical panel | Every 3–5 years | Licensed inspector report |

| Plumbing | Annually | Inspection report, photos |

| Roof | Annually | Inspection report, photos after storms |

Property maintenance tasks for residential properties follow consistent patterns regardless of location. Aligning your schedule to those patterns keeps your coverage valid and your property in good condition.

Pro Tip: Set calendar reminders for every scheduled maintenance task. Missed appointments are the single most common reason Equipment Breakdown claims get denied.

Key Takeaways

Essential maintenance coverage works only when insurance endorsements and routine service plans operate together, supported by thorough documentation at every step.

| Point | Details |

|---|---|

| Coverage is layered, not single | Combine Equipment Breakdown endorsements with routine service plans for full protection. |

| Documentation drives claim approval | Keep receipts, photos, and inspection reports for every system in every property. |

| Standard policies exclude wear and tear | Homeowner insurance covers sudden events only, not gradual deterioration or neglect. |

| Seasonal scheduling protects eligibility | Missed manufacturer-recommended maintenance can void Equipment Breakdown coverage entirely. |

| Service plans are not insurance | Maintenance plans manage predictable costs but do not cover sudden catastrophic failures. |

Why I think most homeowners get this backward

Most homeowners buy insurance and assume they are covered. They are not. Coverage for internal mechanical failures requires an Equipment Breakdown endorsement that most agents never mention unless you ask. That gap is not an accident. It reflects how insurance products are structured, not how property systems actually fail.

What I have seen repeatedly is that the homeowners who get claims paid are the ones who treat maintenance like a business process. They schedule it, document it, and store the records. The ones who get denied are the ones who did the work but kept nothing to prove it. That distinction is entirely within your control.

Landlords face a harder version of this problem. Tenants do not maintain your property. They use it. That means the responsibility for preventive maintenance falls entirely on you, and the consequences of skipping it show up in denied claims and declining property value. A deferred maintenance problem that costs $200 to fix today can cost $8,000 to remediate after a claim denial.

The uncomfortable truth is that essential maintenance coverage is only as good as the habits behind it. The insurance and the service plan are just tools. The documentation and the scheduling discipline are what actually protect you.

— Jennifer

Maddladder's maintenance services support your coverage strategy

Keeping up with scheduled maintenance is the hardest part of making essential maintenance coverage work. Maddladder serves homeowners and landlords across the Kansas City metro area with licensed, dependable maintenance and repair services designed to keep your property systems current and your documentation complete.

Maddladder's home repair and maintenance services cover the tasks that matter most for coverage eligibility: HVAC filter replacements, plumbing inspections, minor electrical repairs, and seasonal system checks. Every service visit produces a dated invoice you can store in your maintenance records. For properties with aging systems, Maddladder's plumbing and electrical services address the highest-risk failure points before they become claim events. Contact Maddladder for a free estimate and get your maintenance schedule on track.

FAQ

What is essential maintenance coverage in simple terms?

Essential maintenance coverage combines Equipment Breakdown insurance endorsements with routine service plans to protect property systems from both sudden failures and scheduled wear. Neither component alone provides complete financial protection.

Does standard homeowner insurance cover mechanical breakdowns?

Standard homeowner policies exclude internal mechanical and electrical failures entirely. An Equipment Breakdown endorsement must be added separately to cover those events.

What happens if I skip scheduled maintenance?

Skipping manufacturer-recommended maintenance can void your Equipment Breakdown coverage. Insurers deny claims when damage results from neglect rather than a sudden internal failure.

Are service plans and home warranties the same thing?

Service plans cover scheduled preventive upkeep and are not insurance. Home warranties vary by contract but generally cover repair or replacement of specific systems. Neither replaces an Equipment Breakdown endorsement for sudden failure events.

How do I prove maintenance was done when filing a claim?

Keep itemized invoices, receipts, and photographs for every maintenance task. Claims get denied when records are missing, even if the work was completed.