TL;DR:

- A home estimate provides an essential, data-backed valuation for buying, selling, refinancing, or tapping home equity.

- Selecting the right type—appraisal, CMA, or AVM—depends on the transaction's financial stakes and accuracy needs.

A home estimate is a professional valuation of your property's current market value, and it is the single most reliable tool for making sound decisions about buying, selling, refinancing, or tapping home equity. Whether you call it an appraisal, a comparative market analysis, or an automated valuation, the core purpose is the same: replace guesswork with a number grounded in real market data. Lenders, buyers, and sellers all depend on this figure. Without it, you are negotiating blind on what is likely your largest financial asset. Understanding why to get a home estimate, and which type to use, is the difference between a transaction that closes cleanly and one that falls apart at the last minute.

Why is getting a home estimate important for buyers, sellers, and lenders?

Getting a home estimate protects every party in a real estate transaction from a different kind of financial risk. The stakes are high enough that skipping this step rarely ends well.

For buyers, an appraisal is the primary defense against overpaying. Mortgage lenders require appraisals to confirm the collateral value of the home before approving a loan. This means the bank will not lend you $400,000 on a home that appraises at $370,000. The gap becomes your problem, not theirs.

For sellers, a pre-listing estimate validates your asking price before you go to market. A listing priced above appraised value will stall. Buyers using financing cannot bridge that gap without bringing extra cash to closing, which most are unwilling to do. Knowing your number in advance lets you price with confidence or make targeted improvements before listing.

For lenders, the importance of home appraisal comes down to collateral protection. Appraisers calculate loan-to-value (LTV) ratios that determine underwriting terms, interest rates, and whether private mortgage insurance is required. The appraisal is the lender's primary risk management tool.

The consequences of a low appraisal are concrete. If an appraisal comes in below the sale price, buyers must renegotiate, cover the difference in cash, or walk away entirely. Sellers face deal cancellations and re-listing costs. Neither outcome is avoidable without an accurate estimate upfront.

Home estimates also matter well beyond the purchase transaction. Refinancing, cash-out home equity lines of credit (HELOCs), estate planning, and property tax appeals all require a defensible, documented valuation. Real estate investors managing multiple properties use periodic estimates to track portfolio value and make decisions about which assets to hold, improve, or sell.

Pro Tip: Before listing or refinancing, pull your permit history and document every major improvement with receipts and photos. Appraisers can only credit what they can verify.

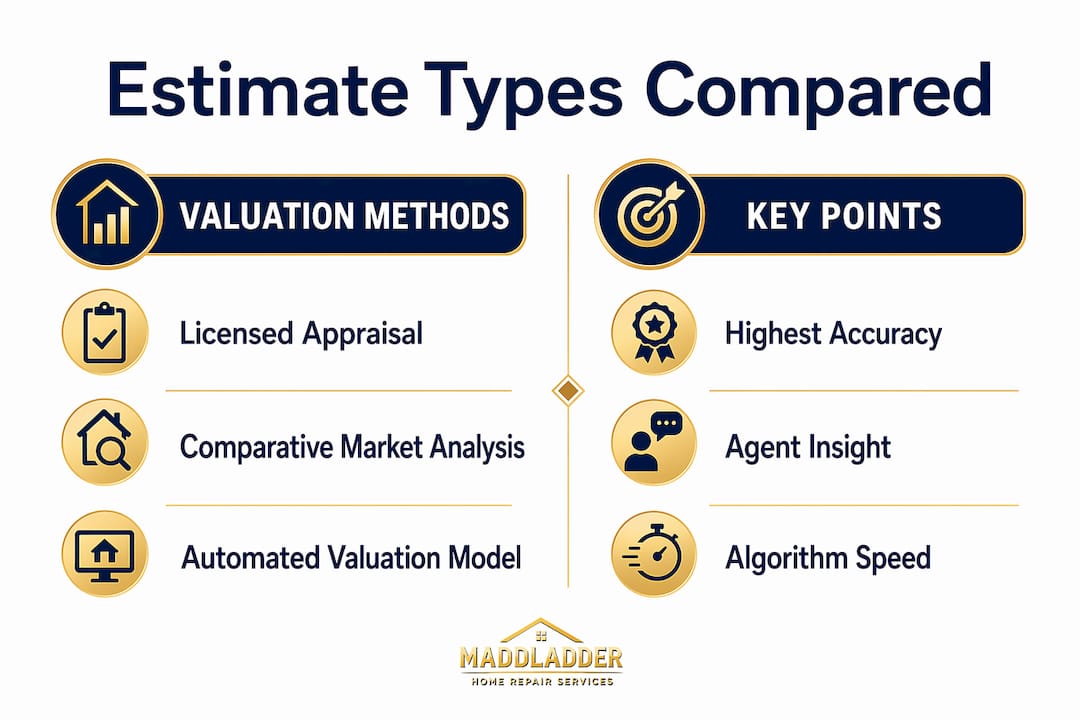

What are the different types of home estimates and how do they compare?

Three distinct valuation methods exist, and choosing the wrong one for your situation is a costly mistake. Each serves a different purpose at a different level of accuracy and cost.

Licensed appraisals are formal, lender-required valuations conducted by a state-certified appraiser. The appraiser physically inspects the property, reviews comparable sales, and produces a report that meets federally mandated USPAP standards including photographs, floor plans, and comparable sales grids. This is the gold standard for any transaction involving a lender. Cost typically runs $300 to $600, and turnaround is three to ten business days.

Comparative Market Analyses (CMAs) are agent-driven assessments based on recent local sales data. CMAs are typically free and aimed at pricing strategy rather than lender underwriting. A skilled agent's CMA can be highly accurate in active markets, but it carries no legal weight with a lender and reflects the agent's interpretation of the data.

Automated Valuation Models (AVMs) like Zillow's Zestimate and Redfin's estimate are algorithm-driven tools that aggregate public records and listing data. They are fast, free, and useful for a quick ballpark. AVMs are not reliable enough for final financial decisions without supplemental valuations. A home with a recent renovation, unusual layout, or limited comparable sales in the area can be off by tens of thousands of dollars.

| Method | Accuracy | Cost | Best For | Who Uses It |

|---|---|---|---|---|

| Licensed appraisal | Highest | $300–$600 | Mortgages, refinancing, legal matters | Lenders, buyers, sellers |

| CMA | Moderate to high | Free | Listing price strategy | Sellers, agents |

| AVM (Zillow, Redfin) | Variable | Free | Initial research, quick reference | Homeowners, investors |

The practical approach is to layer these methods. Use an AVM to get oriented, request a CMA from a local agent when you are preparing to list or buy, and commission a licensed appraisal when a lender or legal matter requires documentation. Matching the valuation method to the decision stage is how homeowners and investors avoid both overpaying for unnecessary appraisals and under-preparing for high-stakes transactions.

Pro Tip: When reviewing your home's estimated value on multiple AVM platforms, check three or four tools and note the range. A tight range signals reliable data. A wide spread signals limited comps and the need for a professional assessment.

How does a home estimate impact refinancing and home equity decisions?

Refinancing without understanding your current home value is like negotiating a salary without knowing the market rate. The appraisal determines everything that follows.

A refinance appraisal assesses your home's current condition and market comps without reference to your original purchase price or contract. The appraiser does not care what you paid in 2019. They care what comparable homes sold for in the last six months. This distinction matters because it works in your favor when values have risen and against you when they have not.

The appraisal directly affects your refinance terms in several ways:

- Loan-to-value ratio: A higher appraised value lowers your LTV, which can qualify you for better interest rates.

- PMI removal: If your LTV drops below 80% based on the new appraisal, you may eliminate private mortgage insurance, saving hundreds per year.

- Cash-out limits: For a cash-out refinance or HELOC, the appraised value sets the ceiling on how much equity you can access.

- Loan approval: If the home appraises below the amount you need to refinance, the lender may reduce the loan amount or decline the application.

Home improvements directly influence refinance appraisal outcomes, but only when documented. Appraisers require documentation of improvements to credit them positively. A new roof, updated kitchen, or finished basement adds value only if you can show permits, receipts, and before-and-after records.

Real estate investors managing multiple properties treat periodic appraisals as portfolio management tools. Knowing the current appraised value of each property informs decisions about which assets to refinance for capital, which to sell, and which to hold. Relying on purchase-era values in a shifted market leads to mispriced assets and missed opportunities.

What factors influence a home's estimated value?

Appraisers and AVMs weigh a consistent set of factors, and knowing them lets you anticipate your estimate and address weaknesses before the appraiser arrives. Appraisers evaluate property size, condition, location, comparable sales, and legal compliance as core inputs.

Location is one of the primary drivers of value, along with comparable sales and documented local market knowledge. Two identical homes on different streets in the same city can appraise at meaningfully different values based on school district ratings, proximity to amenities, and neighborhood trajectory.

| Factor | What appraisers look at | Impact on value |

|---|---|---|

| Size and layout | Square footage, bedroom and bathroom count, functional floor plan | Direct positive correlation |

| Condition and systems | HVAC age, roof condition, plumbing, electrical, foundation | Poor condition lowers value significantly |

| Renovations | Kitchen and bathroom updates, finished spaces, additions | Adds value when permitted and documented |

| Location | School district, neighborhood quality, street position, walkability | Can override physical attributes |

| Comparable sales | Recent sales of similar homes within one mile | Sets the ceiling and floor for valuation |

| Legal compliance | Permits, code compliance, absence of health hazards | Non-compliance can reduce or block financing |

The condition of major systems carries particular weight. An HVAC system past its useful life, a roof with five years remaining, or outdated electrical panels are red flags that appraisers note and adjust for. Addressing these before an appraisal, and documenting the work, is one of the most direct ways to protect your estimate. Maddladder's repair and replacement services are specifically designed for this kind of pre-appraisal preparation.

Assessed value, appraised value, and market value are three distinct numbers that serve different purposes. Assessed value drives your property tax bill. Appraised value is the lender's professional opinion. Market value reflects what a buyer will actually pay in an open transaction. Confusing these three is one of the most common home estimated value questions homeowners ask, and the answer matters for taxes, financing, and sales strategy.

Key takeaways

Getting a home estimate is the foundation of every sound real estate decision, from purchase and sale to refinancing and equity management, and the type of estimate you choose must match the financial stakes involved.

| Point | Details |

|---|---|

| Appraisals protect all parties | Lenders, buyers, and sellers rely on licensed appraisals to prevent overpaying and over-lending. |

| Match method to decision | Use AVMs for research, CMAs for pricing strategy, and licensed appraisals for lender-required transactions. |

| Refinancing depends on current value | Appraisal results directly affect your loan terms, PMI status, and cash-out eligibility. |

| Document improvements | Appraisers can only credit renovations that are permitted and supported by receipts or records. |

| Three values, three purposes | Assessed, appraised, and market values each serve a different function in taxes, financing, and sales. |

What I've learned about home estimates that most articles skip

I have reviewed enough home transactions to say with confidence that the biggest mistakes happen not from ignorance of appraisals but from misplaced confidence in the wrong tool. Homeowners check their Zillow Zestimate, feel good about the number, and walk into a refinancing conversation or a listing decision without ever questioning whether that number holds up under scrutiny. It often does not.

The AVM problem is real. These tools are built on public records and listing data, which means they lag the market, miss interior condition entirely, and struggle with properties that lack close comparables. A home in a neighborhood with few recent sales can show a Zestimate that is off by 15% in either direction. That is a $60,000 error on a $400,000 home. No one should make a six-figure financial decision on that basis.

What I recommend instead is treating the valuation process as a sequence, not a single event. Pull the AVMs first to get a range. Then talk to a local agent about a CMA, especially if you are within six months of a sale or refinance. Commission a licensed appraisal when a lender requires it or when the financial stakes justify the cost. This sequence costs almost nothing extra and eliminates the most common surprises.

The other thing most articles skip: the condition of your home's systems matters more than most owners realize. A fresh coat of paint impresses buyers. A 20-year-old HVAC system concerns appraisers. Prioritize the systems, document the repairs, and you will rarely be surprised by a low appraisal. Investing in property value improvements before an appraisal is not cosmetic. It is financial strategy.

— Jennifer

How Maddladder helps you prepare for a stronger home estimate

Your home's appraised value reflects its condition on the day the appraiser walks through the door. Deferred repairs, aging systems, and unfinished projects all pull that number down. Maddladder serves Kansas City homeowners and landlords with the exact services that move the needle before an appraisal: plumbing and electrical repairs, drywall and trim work, and smart home upgrades like thermostats and security cameras that appraisers increasingly recognize as value-adding features. Whether you are preparing to sell, refinance, or simply want your property in top condition, Maddladder offers free estimates and flexible pricing starting at $75/hour. Contact Maddladder today to get your home ready for its best possible valuation.

FAQ

Why should I get a home estimate before selling?

A pre-listing home estimate confirms your asking price is grounded in current market data, reducing the risk of a deal falling apart when the buyer's lender orders an appraisal. It also identifies condition issues you can address before they cost you a negotiated price reduction.

What is the difference between an appraisal and a Zillow Zestimate?

A licensed appraisal is a formal, lender-accepted valuation conducted by a certified professional, while a Zillow Zestimate is an algorithm-based estimate using public data. Zestimates are useful for initial research but are not accepted by lenders for mortgage or refinancing decisions.

How does a home estimate affect my ability to refinance?

The appraised value from a refinance appraisal sets your loan-to-value ratio, which determines your interest rate, whether you qualify for PMI removal, and how much equity you can access through a cash-out refinance or HELOC.

How often should homeowners assess their home's value?

Most financial advisors recommend reassessing home value every one to two years, or any time you plan a major financial decision involving the property. Markets shift, and an outdated estimate can lead to mispriced listings or missed refinancing opportunities.

Do home improvements always increase an appraised value?

Not automatically. Appraisers credit improvements only when they are permitted, documented, and supported by comparable sales showing buyers pay more for similar upgrades in your market. Unpermitted work can actually reduce value by creating legal and financing complications.