TL;DR:

- Hiring insured handymen offers financial protection for property damage and injuries during projects. Homeowners should verify coverage through a current Certificate of Insurance, ensuring proper policy limits and active dates before work begins. Distinguishing between insured, licensed, and bonded status is crucial for comprehensive risk management on home repair jobs.

Hiring someone to work in your home is an act of trust. But knowing what does insured handyman mean before you sign off on any project is less about trust and more about protecting your finances and your property. Many Kansas City homeowners hear the phrase "insured handyman" and assume it's a general badge of professionalism, when it actually refers to a specific type of financial protection that kicks in when something goes wrong on the job. This guide breaks down exactly what that coverage means, what it does not cover, and the questions you need to ask before any work starts.

Table of Contents

- What "insured handyman" really means for homeowners

- Insured vs licensed vs bonded: key differences homeowners should know

- What a Certificate of Insurance (COI) shows and why you should ask for it

- Certificate holder vs additional insured: what every Kansas City homeowner needs to understand

- How Kansas City homeowners verify and apply handyman insurance for peace of mind

- Our take on the insured vs uninsured handyman decision

- Get the protection you deserve with MaddLadder

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Insured means liability coverage | An insured handyman carries insurance protecting against injury or property damage claims related to their work. |

| Insurance differs from licensing | Licensed refers to legal permission to work, bonding is a financial guarantee, and insurance covers accident risks. |

| Ask for a Certificate of Insurance | Verify the handyman’s valid insurance coverage by reviewing their current COI before work starts. |

| Additional insured adds coverage rights | Being named an additional insured offers homeowners protection and coverage rights beyond simply receiving a certificate. |

| Verify coverage matches work scope | Check that the insurance covers the handyman’s specific tasks and that policies are up to date for your project. |

What "insured handyman" really means for homeowners

When a handyman says they are insured, they are telling you they carry liability insurance, typically general liability insurance, that covers financial losses caused by their work or presence on your property. According to U.S. News, an insured handyman carries general liability coverage to pay for third-party bodily injury and property damage claims arising from their work.

Here is what that actually looks like in practice. Say a handyman is installing a ceiling fan in your living room and accidentally drops a tool that cracks your hardwood floor. Or a client trips over the handyman's equipment bag near your front door and gets injured. General liability insurance is what pays for those repairs or medical bills, not you.

What general liability insurance typically covers:

- Bodily injury to third parties (neighbors, family members, or you) caused by the handyman's work

- Property damage to your home or belongings caused by the handyman's actions or negligence

- Legal defense costs if a lawsuit arises from an incident during the job

- Completed operations coverage for damage that appears after the work is finished

Being insured does not automatically mean the handyman is licensed to perform specific trades. That is a separate credential entirely, and confusing the two is one of the most common mistakes Kansas City homeowners make. If you want to understand the licensed handyman risks around hiring someone without proper credentials, that distinction matters just as much as insurance.

Insured vs licensed vs bonded: key differences homeowners should know

These three words get thrown together constantly, and they are not interchangeable. Each one means something different, and each protects you in a different way.

As Next Insurance explains, licensed, bonded, and insured are separate concepts. "Insured" specifically addresses coverage for accidents and property damage. Bonding is an entirely different financial mechanism.

Here is how to keep them straight:

- Licensed: The handyman has met the state or local regulatory requirements to legally perform specific types of work. In Missouri, licensing requirements vary by trade and municipality. Not all handyman work requires a license, but electrical and plumbing work above certain scopes typically does.

- Bonded: A surety bond is a financial guarantee. If the handyman takes your deposit and disappears, or fails to complete the agreed work, the bond provides a way to recover those funds. It protects you from contractor fraud and non-performance, not accidents.

- Insured: As we covered, this is about liability coverage for injuries and property damage that occur during the job. It protects you from unexpected out-of-pocket costs when something breaks or someone gets hurt.

A handyman can be insured but not licensed. They can be licensed and insured but not bonded. For most home repair projects, you want all three. A contractor who checks only one box is not giving you the full picture. Understanding handyman licensing explained helps you know exactly what credentials to ask about before work begins.

What a Certificate of Insurance (COI) shows and why you should ask for it

Saying "I'm insured" is easy. Proving it takes about 30 seconds. A Certificate of Insurance, commonly called a COI, is an official one-page summary document issued by the handyman's insurance company. It shows you the key details of their active coverage without you needing to read a full insurance policy.

Per Wexford Insurance, homeowners should request proof of insurance via a COI showing coverage type, limits, and policy dates to verify valid insurance before work starts. A legitimate handyman will have this document ready. If they hesitate or can't produce one, treat that as a red flag.

What a COI includes:

- The name of the insured (the handyman or their business)

- Coverage type (e.g., general liability, workers' compensation)

- Policy limits (how much the insurer will pay per occurrence and in aggregate)

- Policy effective and expiration dates

- The issuing insurance company

Pro Tip: When you receive a COI, check the policy expiration date against your project start date. An expired policy is worthless. If the handyman's policy lapses mid-project, you could be unprotected for the latter half of the work.

For minor plumbing or electrical repairs, the stakes around proper insurance verification are especially high because those jobs carry elevated liability risk. A COI gives you a paper trail that holds up if a dispute ever arises.

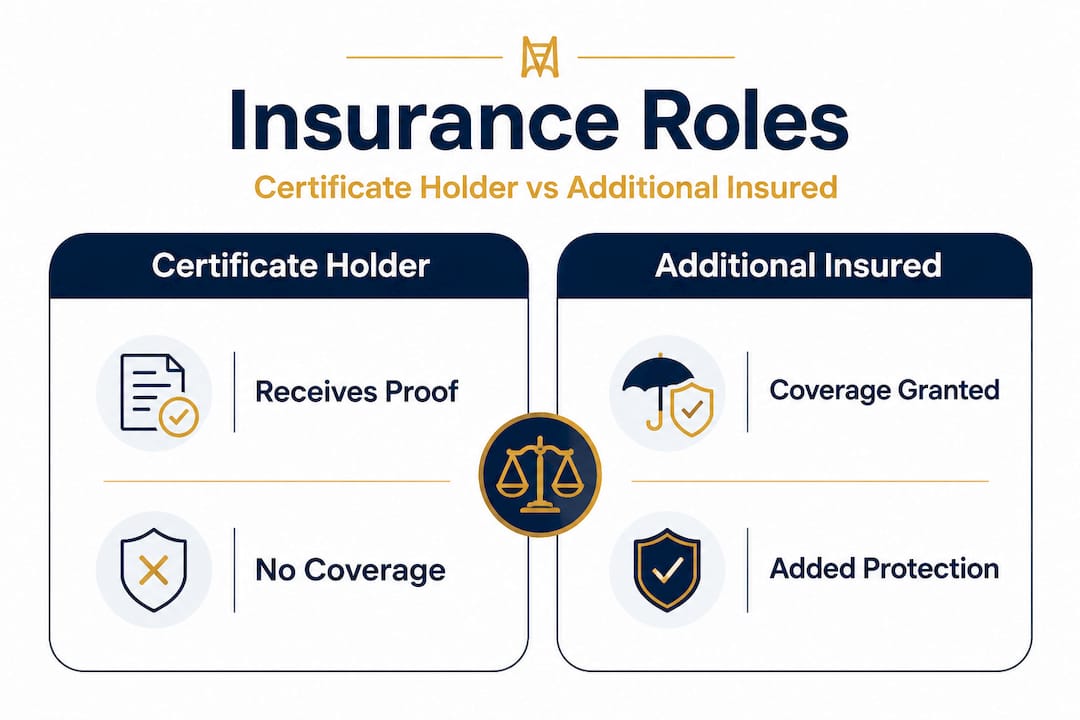

Certificate holder vs additional insured: what every Kansas City homeowner needs to understand

This distinction rarely gets explained to homeowners, but it could cost you significantly if you get it wrong on a high-value project.

When you request a COI from a handyman, you are typically listed as the certificate holder. That sounds official, but it only means you received a copy of their insurance information. It does not give you any rights under the policy. If a claim arises, you have no standing to seek a defense or compensation directly through that insurance.

Additional insured status is different. According to Smart Insured, being listed as an additional insured provides coverage rights through a policy endorsement, while certificate holders receive proof only with no coverage rights.

Here is a quick comparison:

| Status | What you receive | Coverage rights | Best for |

|---|---|---|---|

| Certificate holder | Proof of insurance only | None | Routine small repairs |

| Additional insured | Policy endorsement coverage | Yes, for related claims | Major renovations, higher-risk jobs |

Steps to take for higher-liability projects:

- Ask the handyman if their policy allows additional insured endorsements.

- Request the endorsement in writing before work begins.

- Confirm the endorsement specifically covers the type of work being done.

- Keep the endorsement document with your project records.

For most small jobs like furniture assembly or a grab bar installation, certificate holder status is fine. But if you are hiring for a larger project, understanding the insurance coverage rights difference could matter enormously if a serious incident occurs.

How Kansas City homeowners verify and apply handyman insurance for peace of mind

Knowing what insurance looks like on paper is one thing. Putting that knowledge to work before someone starts drilling into your walls is another.

Harris Insurance is direct on this: do not stop at a handyman saying they are insured. Ask to see a current COI listing general liability and workers' compensation if applicable, and verify the policy is active and relevant for the job.

Here is your practical checklist before hiring any handyman in the Kansas City metro area:

- Request a current COI before any work begins, not after they have already arrived at your door

- Verify the policy dates include your project date, not just a past period

- Check liability limits and make sure they are appropriate for your project scale (a $100,000 general liability limit is very different from $1,000,000)

- Ask about workers' comp if the handyman brings employees or subcontractors onto your property

- Ask about being named additional insured for any project involving structural work, electrical, or plumbing

- Keep a copy of all insurance documents in your home records alongside the project invoice

Pro Tip: A general liability limit of $1,000,000 per occurrence is a reasonable baseline for most residential handyman work. If a contractor only carries $100,000 in coverage and causes significant water damage from a plumbing repair gone wrong, you may find yourself pursuing the rest through small claims court.

Understanding flexible pricing options is also part of the picture. An insured professional may cost slightly more per hour than an uninsured one, but the risk transfer you get is worth every dollar when something unexpected happens.

Our take on the insured vs uninsured handyman decision

Here is an uncomfortable truth most homeowners discover too late: the cost difference between insured handyman services and an uninsured one is rarely as large as people assume. But the financial exposure gap between the two is enormous.

We have seen Kansas City homeowners save $20 an hour by hiring an uninsured contractor, only to face a $4,000 flooring repair bill when that person caused water damage from a botched supply line installation. The math simply does not work in favor of cutting corners on this.

There is also a less talked-about dimension to handyman insurance: it signals professional intent. A handyman who carries proper general liability insurance is someone who has made a real business investment. They took the time to apply, they pay premiums, and they have a financial stake in keeping their work quality high so their rates do not go up. An uninsured handyman carries none of that accountability structure.

What we find most valuable is teaching homeowners to treat insurance verification the same way they treat getting a written estimate. Both are standard. Both protect you. Neither should be optional. The homeowners who skip the COI request are often the same ones surprised to find out the phrase "I'm insured" was never actually verified.

The real protection of insured handyman services is not just the payout if something goes wrong. It is the professional standard it represents before a single nail gets driven.

Get the protection you deserve with MaddLadder

Knowing what insured handyman services should look like is only half the equation. The other half is actually hiring someone who shows up, does the job right, and backs it with real coverage.

At MaddLadder, we serve homeowners throughout the Kansas City metro area with licensed, insured handyman services covering everything from drywall repairs and fixture replacements to minor plumbing, smart home upgrades, and safety installations. We provide documentation upfront so you never have to guess. Whether you need a one-time repair or a recurring home maintenance plan, we offer flexible pricing starting at $75/hour and free estimates so you can make an informed decision before any work begins. Contact us today to schedule your free estimate.

Frequently asked questions

What does it mean if a handyman says they are insured?

It means the handyman carries liability insurance, typically general liability, to cover injuries or property damage caused during their work, protecting you from unexpected financial costs if something goes wrong on the job.

Is an insured handyman always licensed?

No. Being insured only means they carry insurance coverage. As separate legal concepts, licensing confirms legal authorization to perform specific work, and you should verify both independently before hiring.

What is the difference between a certificate holder and additional insured?

A certificate holder receives proof of insurance only with no coverage rights, while additional insured status gives you actual coverage rights under the handyman's policy through a formal endorsement.

Should homeowners ask to see a Certificate of Insurance before handyman work?

Yes, always request a current COI before any project begins so you can confirm coverage types, policy limits, and active dates, giving you documented protection if a claim ever arises.